#1 Trusted, Reliable, Local Roofer

ROOFING INSURANCE

Providing Reliable & Trusted Residential & Commercial New Roof, Roof Installation & Roof Repairs.

We have expert roofers with over 25 years of experience.We are licensed and insured

GET YOUR FREE QUOTE TODAY!!

Roofing Insurance

Roofing insurance is a type of coverage that protects homeowners from losses resulting from roof damage. This insurance covers the cost of repairs to the roof and any resulting damage caused by any issues.

Damage from weather, age, and wear is costly. Roofing protection covers repairs and replacements and interior damage from leaks. Homeowners’ policies may not cover enough, so separate roofing security is important.

It’s important to understand that homeowner’s insurance policies may not cover your roof. Thus, it’s crucial to consider a separate roofing insurance cost for adequate protection. This type of policy can provide the necessary coverage for repairs and replacements.

This blog post will cover the different types of roofing backing, what’s covered, and not what’s not covered. Also, we will discuss the benefits of having this coverage. We will also help you determine whether you need roofing assurance and provide tips on finding the best policy. This post will help provide information so you can make an informed decision.

Benefits of Roofing Insurance

Roofing insurance provides several benefits to property owners, including:

Financial Protection

It provides financial protection in the event of unexpected damage to the roof. Replacing a damaged roof can be expensive, and cheap roofing insurance can help ease the financial burden.

Reduced Risk

Roof insurance reduces the risk of financial loss from unexpected roof damage, letting you focus on other property issues.

Long-Term Savings

A Roofing allowance Claim can help you save money in the long run by covering roof repairs or replacement expenses.

Types of Roofing Insurance

The following are the two primary categories of roofing insurance policies:

Homeowner’s Insurance

Homeowners’ insurance usually covers damages caused by unexpected events like hailstorms and windstorms.

Commercial Property Insurance

Property insurance covers more types of damage that can happen to a building, like roof fires, people breaking things, or water damage.

How to Get Roofing Insurance

If you are looking to get roofing protection, try this simple guide to filing an insurance claim:

Understand Your Roofing Insurance Needs

Think about what kind of coverage you need for your roof. Consider factors such as size, age, and weather in your area.

Research Insurance Providers

Look for insurance providers that specialize in roofing insurance. You can find their research online, check out their reviews, and ensure they are trustworthy.

Compare Coverage and Costs

After researching different cheap roofing insurance companies, compare their coverage and costs. Look for policies that offer the range you need at a reasonable price.

Get Quotes

Contact the insurance providers you’re interested in and ask for quotes. You will Provide them with information about your roof, including its size, age, and location.

Review the Policy

Once you receive the quotes, review the policy. Check that it addresses all your concerns and that you know the terms and conditions.

Buy the Insurance

After buying the insurance, remember to pay your premiums early to avoid coverage lapses.

Keep Your Roof in Good Condition

To ensure your roofing liability insurance remains valid, keeping your roof in good condition is essential. Regular maintenance and repairs can prevent damage and reduce the risk of claims.

How Much Does Roofing Insurance Cost?

For an owner-operator, a Cheap policy costs between $2,500 and $3,500. The premium for good coverage is deductible on your annual gross receipts. It can range from $40.00 per $1,000 to $75.00 per $1,000.

Roofing Contractor Insurance cost

Roofing contractor insurance protects roofing companies against property damage claims. And this applies to third-party injuries too. This policy helps roofing company owners ensure quality work. And help the company avoid financial burdens from roofing accidents.

Roofing contractors like to work with companies with insurance so workers avoid accidents. Some places made it a law that all roofing companies must have insurance.

How to Get Roofing Contractor Insurance

To know how to get your roofing contractor insurance, follow these steps below:

Choosing an Insurance Carrier

Selecting the right business insurance carrier is crucial for any roofing business. Conducting your operations can impact your level of protection and peace of mind. There are a few key factors to consider when choosing an insurance carrier to ensure you get the best roofing business insurance.

Choosing an insurance carrier with specialized roof contractor coverage is crucial. Not all carriers have roofing industry expertise despite offering roofing contractors liability insurance. Opting for a carrier guarantees their understanding of the unique risks that your business faces. By doing so, you can trust that your insurance coverage will meet your specific needs.

Another important factor to consider when choosing a carrier is financial stability. You want to work with a carrier with a good industry reputation. And a history of providing reliable insurance coverage to their clients.

This will ensure that you receive quality service. You can research online reviews and ratings to understand the carrier’s reputation. Also, you can ask for referrals from other contractors in your industry.

Also, You want to work with a carrier that communicates throughout the insurance process. This includes helping you understand the coverage options available. And also explaining any exclusions or limitations in the policy.

Completing the Application Process

Completing the application process is the next step toward obtaining roofing contractor insurance. This involves submitting an application and answering a questionnaire from the insurance company.

The information provided in the application is essential to determine the type of coverage and the cost of the insurance policy. The application process begins with providing basic information about your company, such as its name. It will also need your location, type of business, and how much revenue it generates.

The next step is to provide details about your business operations. This includes the types of roofing services you offer, the materials you use, and the safety measures you have in place. Your insurer will use this information to assess the risk associated with your business to determine the best coverage for you.

Additionally, you must disclose whether your company has made any insurance claims before. Answering all the application questions and avoiding discrepancies are important.

Underwriting Process

Once the insurance company receives your completed application, they will begin underwriting. When applying for insurance, the underwriting process assesses your roofing business insurance risks.

The insurer checks past claims, verifies the information provided, and considers various factors. After the assessment, the underwriter sets the insurance premium based on the risk.

They may also suggest ways to reduce risk, such as implementing better safety procedures. Working with the insurance company during underwriting is essential to address any concerns. And get the best coverage at the most reasonable cost.

Premium Payment

The final step in obtaining roofing contractor insurance is premium payment. The insurance premium must be paid once the application has been approved in order to ensure coverage and protect your business from general liability insurance claims.

Most insurance companies offer payment plans that allow clients to pay their premiums in installments. It is important to note that some insurers prefer third-party payment. While others must pay in full during application. Discuss payment options with your insurance carrier to ensure you select a convenient payment plan for you and your roofing businesses.

What Kind of Insurance Should a Roofing Contractor Have?

There are many types of insurance every roofing contractor should have, and we will consider some of the necessary ones.

Commercial Property Insurance

A roofing business owner’s policy (BOP) typically combines general liability coverage and commercial property insurance at a discounted rate, making it a cost-effective insurance option for roofing professionals. This policy can cover property damage, such as damages to the facility storing generators, ladders, shingles, etc., caused by vandalism or windstorms. Additionally, a BOP may include liability coverage for some small businesses, covering third-party property damage or bodily injury to non-employees.

The property owner will have peace of mind knowing the business owner has an insurance policy to deliver ‘s policy covers that Protects businesses by covering damages to their property. These damages may be from fire, theft, or natural disasters.

This type of insurance is common insurance for manufacturing and construction companies. Commercial property insurance covers any damage to insured properties during roofing construction. And includes damage to equipment and tools.

All insurance companies will consider the value of equipment, tools, and building.

Injury liability coverage

This roofing contractor insurance protects the workers and general liability insurance coverage pays the medical cost of injured people after a work accident.

The injury liability covers bills like hospital costs, emergency care, and other care expenses when hurt. Legal judgments and counsel are also included in case of a lawsuit for or against you. The policy also pays for other things like funeral costs if someone dies.

The hurt person’s pain, suffering, and lost income if they can’t work because of their injuries are also covered.

Property Damage General Liability Coverage

Property damage general liability coverage includes the cost of damage to someone’s property after an accident. Suppose your roof contractors damage someone’s property, like cars, buildings, or trees.

In that case, the insurance company will cover the cost of any damage and legal fees if any legal actions come.

The insurance company will pay the other party the amount stated in your policy after an accident.

General liability insurance for roofing contractors covers third-party property damage or bodily injury to non-employees, such as a person injured by a dropped tool. It also provides liability coverage for issues like leaks in a new roof and libel or other advertising injuries. In some cases, roofing liability insurance coverage may be appropriate for roofing contractors who consult with customers and recommend specific products or treatments.

General liability insurance is crucial coverage for roofing contractors, as it provides a safety net against a variety of potential risks and liabilities that can arise during the course of their work. Here are some of the key aspects of general liability insurance coverage for roofing contractors:

Bodily Injury Liability: This coverage protects roofing contractors in case a third party, such as a client or passerby, is injured due to the contractor’s work. For example, if a ladder falls and injures a person, general liability insurance will cover the medical expenses and legal fees associated with the claim.

Property Damage Liability: If a roofing contractor accidentally causes damage to a client’s property or neighboring property, general liability insurance will cover the costs of repairing or replacing the damaged items. This may include damage caused by falling debris, tools, or equipment during a roofing project.

Products and Completed Operations: This coverage protects roofing contractors against claims arising from faulty workmanship or defective materials used in a completed project. For example, if a newly installed roof leaks and causes water damage, the general liability insurance will cover the costs of repairing the damage and any legal fees resulting from the claim.

Personal and Advertising Injury: General liability insurance also covers claims of libel, slander, or copyright infringement related to a roofing contractor’s advertising or promotional materials. For instance, if a competitor claims that your advertising materials contain false or misleading information, your general liability insurance will cover the costs of defending against the claim and any damages awarded.

Legal Defense and Judgments: In the event of a lawsuit, general liability insurance covers the costs of legal defense, including attorney fees, court costs, and any settlements or judgments awarded to the claimant. This protection is crucial for roofing contractors, as legal fees and damages can be financially devastating for a small business.

It is important to note that general liability insurance does not cover injuries to the roofing contractor’s employees; this is covered by workers’ compensation insurance. Additionally, general liability insurance does not cover damage to the contractor’s own tools, equipment, or vehicles, which would be covered under commercial property insurance or commercial auto insurance, respectively.

General liability insurance is a vital component of a roofing contractor’s risk management strategy, providing protection against a range of potential liabilities and ensuring the financial stability of the business.

Advertising injury liability coverage

This type of roofing contractor insurance is rare in the industry but very necessary. Suppose a roofing contractor or any company publishes ad content that damages the reputation of another company or puts them at a loss.

In that case, the insurance company will pay for the lost income. Advertising injury liability covers slander, invasion of privacy, and copyright infringement will also be lost. It protects against claims and legal expenses related to such damages.

Professional liability insurance

It is the most common insurance policy for businesses that give out service for a fee. The insurance protects roof contractors and other workers in cases where the client sues them for an alleged mistake or error.

Professional liability insurance covers professional negligence. It also covers breach of contract, errors, misconduct, and failure to deliver on time as promised. This insurance does not cover injuries or damage to properties.

Compensation Insurance and Medical Bills Insurance

Compensation insurance for roofers, also known as workers’ comp insurance, is a type of coverage that protects employees in the case of an accident or bodily injury while working on a roofing job. This insurance is required in almost every state for roofing businesses, whether or not they have employees. It helps cover work injury costs that health insurance might deny, such as work-related medical expenses

From the name, this health insurance policy pays workers who get injured or become ill as a direct result of the job. The policy covers workers comp medical expenses and current and future bills for injuries caused by the job. It also covers lost wages and salaries, disability benefits, and death compensation.

Your compensation insurance which pays for medical bills and compensation if you get hurt at work doesn’t always cover every type of bodily injury. If you’re hurt because of a fight at work, using drugs or alcohol, or while traveling to or from work, your health insurance may not cover those injuries.

Commercial Auto Insurance

Commercial auto insurance covers any damages done to commercial vehicles used in business.

Commercial Auto insurance pays for three things if you get into a car accident:

- It pays for fixing your car if it gets damaged in an accident.

- It pays for any medical expenses you might have if you get hurt in an accident.

- It pays for any legal fees you might have if someone sues you because of the accident. This insurance is for contractors as they transport their tools from place to place.

How Much Does Roofing Contractor Insurance Cost?

There is no fixed cost for roofing contractor insurance as it differs from state to state. Also, every insurance company has the amount their clients get to pay for each insurance type.

Some types of insurance policies and their cost are:

- Compensation and medical bills insurance – $750 to $810 monthly and about $9,690.

- Commercial auto insurance – $120 to $140 monthly and $1,685. Yet, there is a limit of $1 million.

- Professional liability insurance – $80 to $85 monthly and about $1,000 yearly.

- Commercial property insurance – $31 to $55.

- Property damage insurance – $800 to $810 or $9,690.

Roofing Insurance Claim Process

Roofing insurance claims work by providing coverage for unexpected damage to your roof.

Following these steps, you can file an insurance claim for roofing damage and get the necessary repairs.

Steps Involved in the Roofing Insurance Claims Process

The roofing insurance cover claims process is always challenging as there are many steps involved; we will look at some of these steps involved.

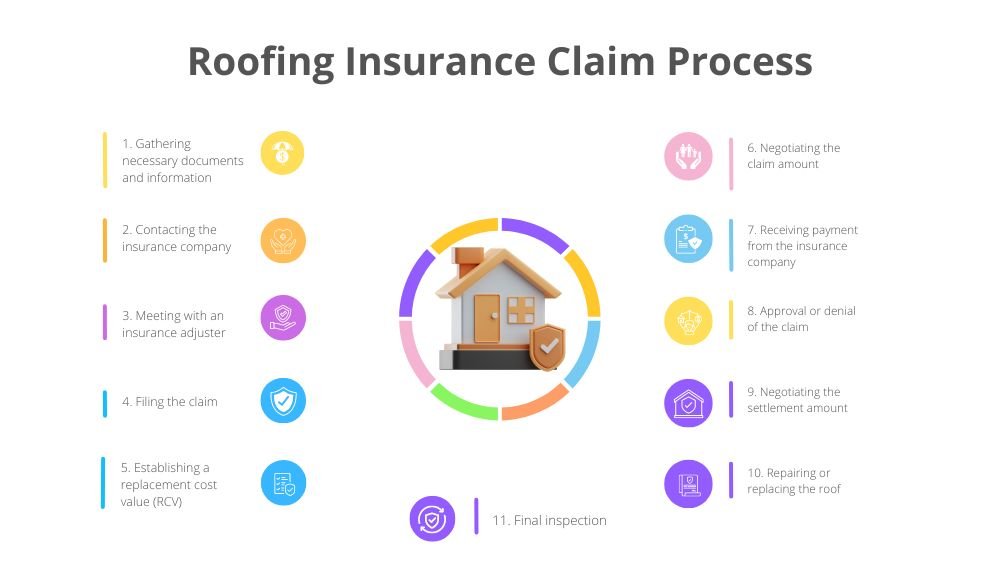

1. Gathering necessary documents and information

The first step towards filing a roofing insurance claim is to assess the damage done to the roof. And you should know the cause and the amount of damage done. You can use a ladder for a more detailed and thorough look at the roof. Look out for damaged gutters, missing or loose shingles, cracked or dented roof parts, or leaks inside the house.

Gather all evidence, Previous insurance policy, and information with necessary documents. Including your house paperwork to help the insurance company understand the damage.

2. Contacting the insurance company

Contact your insurance company and let them know about your situation. The Company will also help you with information on the requirements needed for claims and the process involved.

Informing the insurance company will help you know if you are filing for partial repair or going for an actual cash value of the damage. This is also the best time to ask your agent about the insurance coverage you expect.

3. Meeting with an insurance adjuster

Contacting your insurance company as soon as you notice any damage to your roof is essential to start the claims process. This will help ensure that you receive the necessary coverage and repairs.

After filing your roofing contractors insurance claims, the company will send an adjuster to the damaged roof. This adjuster will review all parts of the roof and the damage done before verifying the information you provided.

To get a better deal or be safe, call a professional roofing contractor to come by for an inspection with the adjuster. The contractor will offer professional advice and even convince the insurance adjuster of the amount of damage done.

4. Filing the claim

After assessing the damage, you must file a claim with your insurance company. You must provide all necessary information, including photos of the damage and the adjuster’s estimate.

5. Establishing a replacement cost value (RCV)

Some homeowners prefer a repair coverage policy, while others prefer actual cash-value coverage. The repair coverage gives full reimbursement for a new roof, while the actual cash value considers the age of the roof and the depreciated value. No matter the type of coverage a homeowner paid for, the insurance claim process will establish a replacement cost value of the damaged roof. This can be the exact market value or lesser.

6. Negotiating the claim amount

After establishing a replacement cost, the homeowner either agrees with the value or negotiates for a higher cost. The insurance company will likely determine the final cost depending on the review by their adjuster. While your private roofing contractor may give you a more accurate quote.

7. Receiving payment from the insurance company

After the homeowner and the insurance company conclude, the latter will send a payment for the roof repair. The fee may come after you make a claim; it may take weeks in most cases, so you may need to fix your damaged roof until the repair work can start.

8. Approval or denial of the claim

The Insurer may approve or deny your roof insurance claim. If The Insurer approves your claim, they will cover the cost value. But, the claim can get rejected if the repair cost exceeds your policy limit or if your negligence causes damage. Additionally, filing many claims may result in the denial of your claim by The Insurer.

You can appeal to the insurance company to make changes if they deny your roofing insurance policies.

9. Negotiating the settlement amount

You must negotiate with your adjuster to determine the settlement if the claim gets approved. Most payments are undervalued, so you should ensure the agreed-upon amount matches your total cost.

10. Repairing or replacing the roof

If your claim gets accepted, contact a professional roofing contractor to either repair or replace the damaged roof. The contractor will set a time frame for the project, and all materials will be at the property site. It is advisable to ensure the roofing contractor works according to their schedule, as there will be inspections.

11. Final inspection

A final Inspection is always done after the claim gets paid. Many believe insurance companies will pay for roofing repairs without inspecting the house. This is false. Insurers follow up to make sure after payment. The funds are used as agreed.

Factors Affecting Roof Insurance Claims Process

Some factors will affect or influence your roof insurance claim process; these factors include:

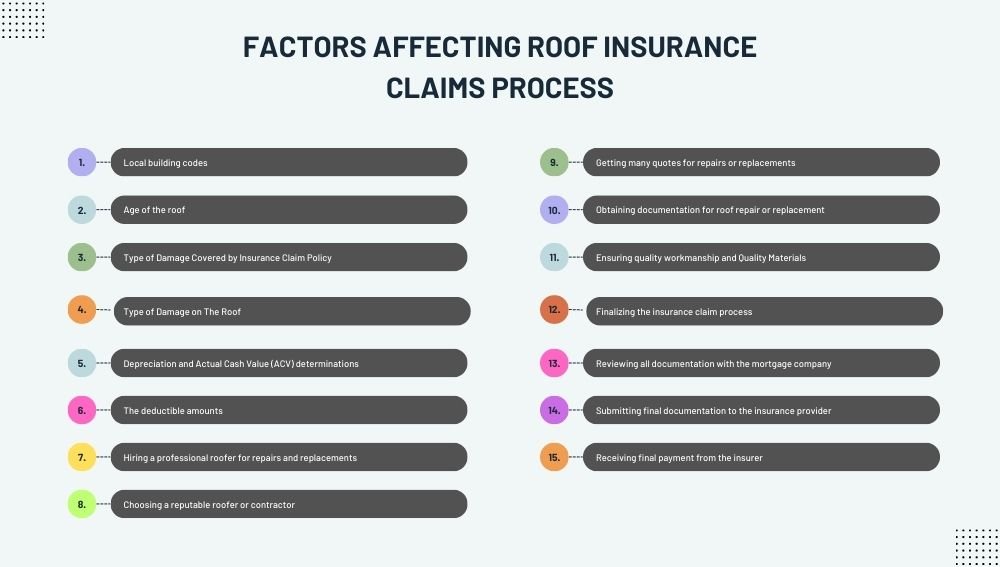

● Local building codes

Most Governments set laws for building and repairing structures called local building codes. If your roof gets damaged and does not follow the codes, the insurance company may ask you to update it to current standards.

● Age of the roof

The age of your roof is one of the most significant factors determining how the insurance process will go. Older roofs are susceptible to damage as the material depreciates as time goes on compared to newer ones.

Also, insurance companies will consider the roof’s age before approving or denying any insurance claim.

● Type of Damage Covered by Insurance Claim Policy

There are two types of damages covered by an insurance policy; the first is damage from a covered loss, and the other is damage from wear and tear. Covered losses include damages caused by rain, snow, storm, faking tree branch, wind, or fire. While wear and tear have to do with damages caused by the failed structure.

Some policies only cover loss, some deal with wear and tear, and others cover both. Knowing your policy type will help with your roof insurance claim process.

● Type of Damage on The Roof

Not all types of damages on the roof get covered by insurance. Insurance covers damages from explosions, fire accidents, theft, vandalism, and weather. Vehicle accidents, lightning strikes, and falling objects are also covered.

Insurance does not cover damages caused by normal wear and tear or unresolved maintenance issues.

● Depreciation and Actual Cash Value (ACV) determinations

Insurance companies calculate property value by subtracting depreciation from replacement costs. This cash value factor will help the insurance company to avoid overpaying the homeowner.

● The deductible amounts

The deductible amount is the amount a homeowner pays an insurance company for an insurance claim. The deductible is the cost of any damage before your insurance coverage takes over.

● Hiring a professional roofer for repairs and replacements

Contractors have insurance policies covering roof repair for damage, influencing your insurance. Insurance companies will prefer an insured roofer. As they will not have to pay for future replacements in case of accidents when the project is ongoing.

● Choosing a reputable roofer or contractor

A reputable roofer or contractor should be someone of integrity who will not provide high costs for the insurance company. Besides providing accurate quotes, contractors will better fix the damaged roof.

● Getting many quotes for repairs or replacements

Supplying many roof repair and replacement quotes to the insurance company will only prolong the claim process. The company will need more time to review the paperwork. Providing many quotes will also create distrust between you, the homeowner, and the insurance company.

● Obtaining documentation for roof repair or replacement

Needs and requires homeowners to present documents of the damaged roof for repair and replacement. The insurance company will not approve your claim if no records are acting as evidence of the damages. The sooner you present your documents, the sooner they support your claim.

● Ensuring quality workmanship and Quality Materials

Having a reputable and professional roofer or contractor for your roof is one thing; using quality materials for the job is another. With quality workmanship and material, the insurance company will ensure there will not be damages due to wear and tear.

● Finalizing the insurance claim process

The insurer finalizes the claim process after reviewing documents and approving the damage. This stage may only happen if the above factors are considered or if some issues harm the insurance claim.

● Reviewing all documentation with the mortgage company

The insurance company will review mortgage documentation to prevent disappearing with repair money. This review factor is essential to avoid financial problems between the homeowner and the lender. All submitted documents from the homeowner must match the ones from the mortgage.

● Submitting final documentation to the insurance provider

Submitting final documentation affects your insurance claim process. Final documents increase your chances of success. Gather all evidence and documents before filing claims to any insurance company.

● Receiving final payment from the insurer

The insurance company will issue the final payment to the homeowner once they review and approve the documents. In cases where the house is still under mortgage, the company will share the check with the homeowner and the lender. The company may issue the total money to the lender in an escrow account until it is time to pay for the repairs.

Roofing Damage Insurance Claim

Insurance companies cover roof damage caused by natural events such as storms, falling trees, or fires. If you have a homeowners insurance policy, it will pay for repairs. Most homeowners insurance policies do not cover roofing damages caused by poor maintenance or neglect.

Here are 4 simple steps to follow when dealing with roofing damage and insurance:

Know your policy coverage

Review your insurance policy to understand specific coverage and corresponding deductibles.

Document the damage

Take notes and pictures of the damage’s severity and contact your insurance company immediately to file a claim within the set time limit.

File the Claim

Submit your insurance claim to the company and let them run their Investigation before collecting it.

What Kind of Roof Damage Gets Covered by Insurance

Damage caused by hail, wind, and fire is often included in standard insurance policies. Hence, if your roof requires repairs after damage from hail or a fallen tree, your insurance coverage helps cover the associated costs.

Common Types of Roofing Damage Claims

There are five types of roofing damage claims:

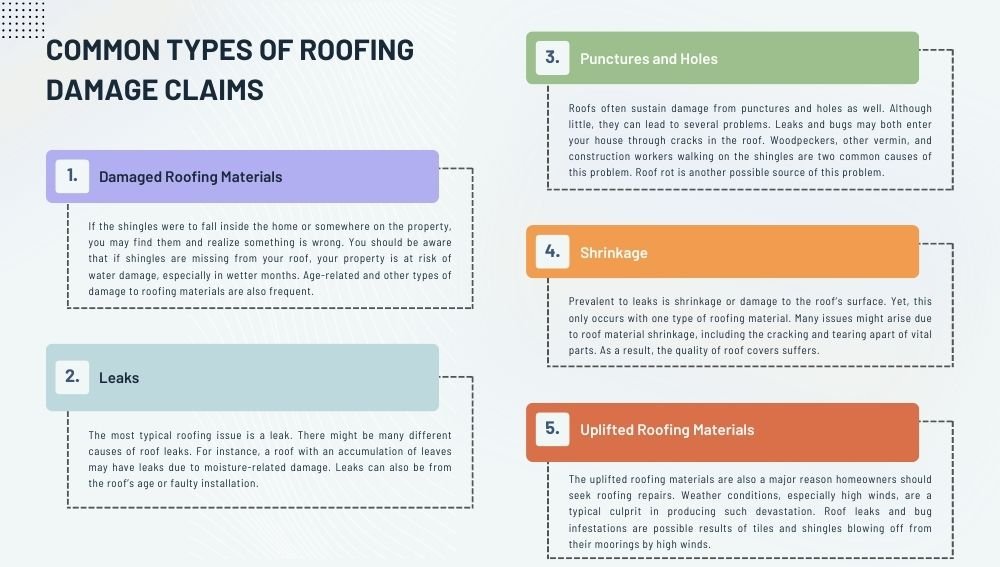

1. Damaged Roofing Materials

Missing materials are another typical type of roof damage. Lack of roofing materials, such as shingles and covers, can cause many problems, including leaks. The most obvious sign of roof deterioration is missing tiles or shingles.

If the shingles were to fall inside the home or somewhere on the property, you may find them and realize something is wrong.

You should be aware that if shingles are missing from your roof, your property is at risk of water damage, especially in wetter months. Age-related and other types of damage to roofing materials are also frequent.

2. Leaks

The most typical roofing issue is a leak. There might be many different causes of roof leaks. For instance, a roof with an accumulation of leaves may have leaks due to moisture-related damage. Leaks can also be from the roof’s age or faulty installation.

3. Punctures and Holes

Roofs often sustain damage from punctures and holes as well. Although little, they can lead to several problems. Leaks and bugs may both enter your house through cracks in the roof.

Woodpeckers, other vermin, and construction workers walking on the shingles are two common causes of this problem. Roof rot is another possible source of this problem.

4. Shrinkage

Prevalent to leaks is shrinkage or damage to the roof’s surface. Yet, this only occurs with one type of roofing material. Many issues might arise due to roof material shrinkage, including the cracking and tearing apart of vital parts. As a result, the quality of roof covers suffers.

5. Uplifted Roofing Materials

The uplifted roofing materials are also a major reason homeowners should seek roofing repairs. Weather conditions, especially high winds, are a typical culprit in producing such devastation.

Roof leaks and bug infestations are possible results of tiles and shingles blowing off from their moorings by high winds.

Homeowners Insurance Policies – Roofing Damage

Homeowners’ insurance policies cover damage to your home, including damage to your roof. But, coverage may vary depending on your policy type and the damage’s cause.

Types of Policies

There are 8 types of homeowners insurance policies:

These policies include; Broad Form, Comprehensive Form, Basic Form, Unit-owners Form, Mobile Home Form, Special Form, Contents Broad Form, and Modified Coverage Form.

Understanding Your Policy

You must grasp the coverages and exclusions of your homeowner’s insurance policy. Go through your insurance policy documentation and contact your provider with any queries.

Check whether coverage restrictions exist, such as a monetary amount the insurance company will pay for roof repairs. Or if there are any exclusions linked to roof damage.

Exclusions in Homeowners Insurance Policies

There may be situations or damages that aren’t covered by homeowners insurance. Standard exclusions in Homeowners insurance plans include damage from natural disasters like floods. Also, earthquakes and everyday wear and tear. Insurance companies may also choose not to pay for losses caused by hurricanes and tornadoes under some plans.

Reading your policy’s exclusions will help you avoid any surprises down the road. Consider obtaining more coverage if you live in a region prone to floods or earthquakes.

Roofing Damage Insurance Claim: Everything You Need to Know

The Claims Process

Filing an insurance claim for roofing damage can feel overwhelming, but it doesn’t have to be. Start by calling your insurance company as soon as you notice the damage. They will ask for details like your policy number, the damage’s date, and what caused it. Keep track of all your conversations with your insurer by taking notes or saving emails.

Once you’ve reported the damage, the insurance company will send an adjuster to assess the damage. It’s essential to be present during the assessment to ensure all damage gets accounted for. The adjuster will then estimate the repair cost, determining the amount of your insurance payout.

Assessing the Damage for Roofing Insurance Quote

Assessing the damage to your roof is an essential step in getting a roofing contractors insurance quote. Inspect your roof for any signs of damage, such as missing or broken shingles, dents, or cracks. You can also hire a roofing contractor to perform the assessment. Ensure you take pictures of the damage to provide evidence to your insurance company.

Filing an Insurance Claim for Roof Damage

When filing a roof damage claim, you must provide all information to your insurer. This includes the date of the damage, the cause of the damage, and the estimated repair cost. You may also need to provide pictures of the damage. And Keep any communication records with the insurance company.

Working With an Insurance Adjuster or Public Adjuster Negotiating the Claims Settlement Amount

An insurance adjuster is a professional who will assess the damage to your roof. And an Insurance adjuster determines the payout for your insurance claim. Working with your adjuster is crucial to ensure that all damage gets accounted for. And you receive a fair settlement amount. If unsatisfied with the adjuster’s estimate, you can hire a public adjuster to negotiate.

Receiving Actual Cash Value

Actual Cash Value (ACV) is the amount you’ll receive from your insurance company for the damage to your roof. It considers the depreciation of your roof and any other factors that may reduce its value.

Common Roofing Insurance Claim Mistakes to Avoid

Homeowners must correct mistakes when filing roof insurance claims to avoid denial or delays. These mistakes include:

● Waiting too long to file the claim

Insurance companies have a time limit for filing claims, usually a year after the roof damage. It is best to file the claim when the damage is still new and there is still fresh evidence. The longer you stay before filing the claim, the harder it will be to convince the insurance company of the damage.

● Failing to document the damage

Having a good record or documentation of the damage is one mistake people make when filing roof insurance claims. Having a document will help the insurance company to know the extent of the damage and also help keep the record in case for future purposes.

● Not understanding your policy

Knowing your policy and what it covers will help you protect your house, especially your roof. You need to understand your policy to see the damage covered by the policy. You should read the policy contract and talk to an agent for help.

● Not communicating with your insurance company

People think filing a claim means the insurance company handles roof repair and replacement. You must communicate with the insurance company, keep track of your claim and follow them up. You can always send emails or call the company for feedback.

FAQs

● Should I file an insurance claim for my roof?

If you have an insurance policy covering your roof, you can file a claim in case of any damage. And the insurance will help remove some financial burden from you.

● Roofer wants me to sign over the insurance check.

Sometimes, it is not advisable to sign over an insurance check or even review it because of fraud. Yet, when you have a reputable roofer, reviewing and signing over an insurance check will help your roofer avoid insurance fraud. And help you review your payment check.

● Roofing companies that work with insurance claims

Most roofing companies now work with insurance claims to help both parties get the exact claim without cheating. Getting a roofing company that works with insurance claims will fix the damaged roof within the time frame.

● Will insurance cover a 20-year-old roof?

Some insurance companies refuse to cover houses with roofs up to 20 years old. And this is to limit the damages and coverage they will get, while others allow 20-year-old roofs that pass insurance.

Conclusion

The claim is very tedious for filing roof insurance as it involves many processes, documents, inspections, and steps. Filing your insurance claim will be easy with the steps outlined above.

A roofing damage claim can be a significant headache for homeowners, but with an understanding of the claims process, it doesn’t have to be. With some preparation and patience, you can file an insurance claim for roof damage and get the necessary repairs.

Also, for Roofing Insurance Claim Process, Your insurance company uses a roofing insurance cost claim process to investigate the damage. After the Process, you can claim reimbursement.

The roofing insurance claim process involves many steps and can be very complicated. Here are steps that will help you understand the roofing process, including how to make and submit an insurance claim.

Roofing insurance protects property owners against unexpected damage to their roofs. Roofing insurance is like having a superhero on your side. Your roofing insurance claim safeguards your property, mind, and wallet. By learning about roofing insurance cost and how to get it, you can also be a property owner superhero!

Finally, roofing contractor insurance is essential to any construction company considering the benefits. As discussed in the content, these benefits include protection for workers and their tools. Also, it helps relieve companies’ financial burdens and fulfill legal obligations. While choosing insurance coverage, it is best to select a suitable insurance carrier who will make the whole process easier for you.

Every household may have roof damage at any moment. Roof damage may result in significant repair or replacement costs, but insurance can ease some financial strain.